If you pay attention to local and state news headlines, you’ve heard about check washing. The Pennsylvania State Police have previously issued warnings to Pennsylvania residents to beware of criminal activity. If you’re an individual or a business that frequently sends checks in the mail, read on to learn how to best safeguard yourself from check washing, as well as what legal recourse you might have.

frequently sends checks in the mail, read on to learn how to best safeguard yourself from check washing, as well as what legal recourse you might have.

What is check washing?

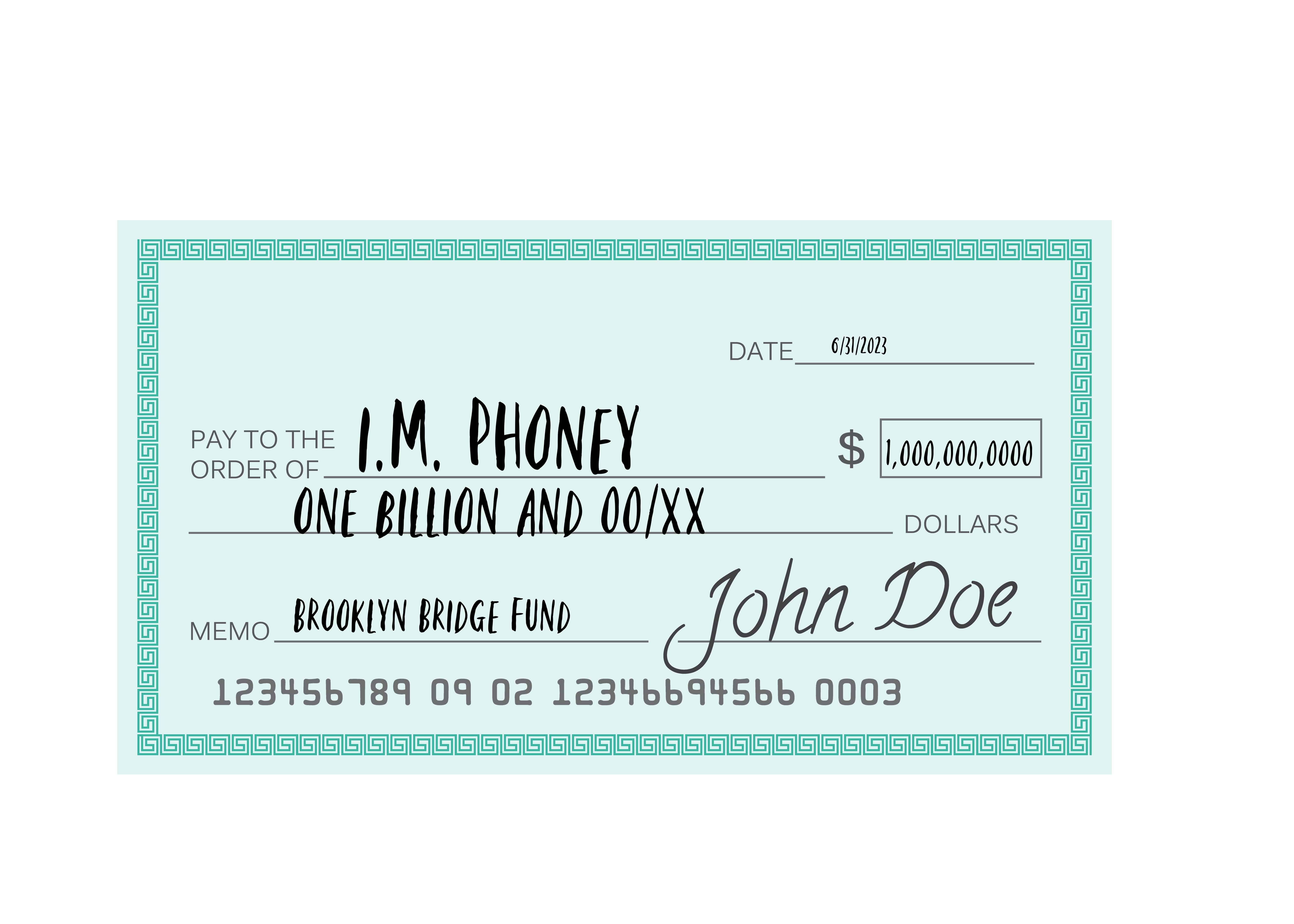

In case you’re unfamiliar with check washing, it’s the act of changing the payee and/or value information of a check and then depositing the funds into an account. The recipient may or may not be intended, and the check can be augmented through a chemical process, or copying or scanning and reprinting. According to the U.S. Postal Inspection Services, more than $1 billion in counterfeit checks and money orders are recovered every year.

Check washing often occurs when a check is stolen from a personal mailbox, but it can also be taken from a business mailbox with a key and even certified USPS mailboxes (the big blue ones) using glue traps.

Beyond a one-time event, criminals can use personal information found on checks to wreak more havoc online, with reports of new loans, bank accounts, and lines of credit being established in a check washing victim’s name. While online banking has removed much of this risk, you may still be the victim of a check that never arrives and is fraudulently deposited into someone else’s account.

If this happens, what can you do? And what about the financial institution that cashes the checks – are they liable?

Liability and recourse in check washing

Make no mistake – check washing is fraud and possibly identity theft. Just one of several forms of check fraud, banks have been overwhelmed and thus slow to respond.

According to the Uniform Commercial Code Section 4-401, the term “properly payable” is used to describe how the paying or drawee bank may only process checks which are not counterfeit or altered. The liability of determining whether the check is unaltered and legitimate falls on the bank of first deposit or payee bank, i.e., the financial institution for the customer depositing the check, who is typically the person committing or connected with the crime of check washing. However, the UCC further dictates that the drawee bank has a deadline until midnight of the next banking day to return the check without processing or paying it.

A 2021 case, “Provident Savings Bank v. Focus Bank” showed how this law plays out, as Focus Bank, the drawee bank, failed to return an electronically duplicated $150,000 check after the midnight deadline. In addition, because the second check was discovered on Focus Bank’s customer’s account with a different payor, the court questioned whether or not it was an alteration or a counterfeit. Ultimately, the court concluded that Provident Savings Bank did not breach the presentment warrant and was not liable, as the evidence from Focus Bank was “insufficient to establish that the check was altered.”

If you’re an individual who is the victim of check washing, you are not liable for the withdrawn funds. Nonetheless, you should report it to your bank as soon as possible, within 30 days of receiving your bank statement. As noted above, the banks must investigate reported fraud and sort out which institution is liable for the loss, but due to the high volume of cases, it may take time to refund your money. According to the American Bankers Association, you may request a “provisional credit” while you wait.

In addition, you can file a report with your local or state police department, as well as the United States Postal Inspection Service.

How can you prevent check washing?

While less prevalent than in previous decades, more than half of Americans are still writing checks. To help prevent your checks from being washed, you can:

- Stop sending checks using your home mailbox and even USPS boxes (unless it’s right before the end of day pickup), and instead, drop your check off inside the post office in the slots; consider using electronic bill pay for added security (although it can also be vulnerable); also collect your daily mail as quickly as possible, rather than letting it sit.

- Monitor your bank accounts and audit your monthly bank statements to look for suspicious or unauthorized activity.

- Make your checks more secure with non-erasable blue or black gel ink, which better soaks into paper checks; consider ordering checks with added security features.

Banks can employ various tools and services like AI technology to help them spot fraudulent checks, protecting their clients and their financial institutions.

Legal representation for check-washing victims

If you are a business that was victimized by check washing or a banking institution embattled in liability, please reach out to a member of our Bankruptcy & Creditors’ Rights team to see if we can help.